Strategy 3 – Is two better than one? It’s certainly more than one…

Let’s turn it up by one. We’ve got two indicators, a trailing ATR stop, some daily charts, profit factors between 2-5 one different asset types, and some ponderings.

Disclaimer: the following post is an organized representation of my research and project notes. It doesn’t represent any type of advice, financial or otherwise. Its purpose is to be informative and educational. Backtest results are based on historical data, not real-time data. There is no guarantee that these hypothetical results will continue in the future. Day trading is extremely risky, and I do not suggest running any of these strategies live.

Greetings from Puerto Vallarta! Lucky for you, this post is coming to you digitally and not covered in the permanent sweat that seems to cling to you the closer you get to the equator. My wife, the toddler, and I flew out from Georgia (the US state, not the country) a few days ago and have been getting settled in this week. This is our first time in Mexico and traveling out of the country with the little man. So far, it has been awesome. The food is fantastic, the sun is ever-present, and the water is warm. I could do without the panhandling, but if you have ever traveled out of the country, you know this is common in some countries. Unless you are rich and you want to avoid the real world. Then, I am sure there are ways to travel and keep your blinders on. To each their own.

Anyway, I got sidetracked for a few days when we arrived, so this article is a couple of days late. With any luck, this should be the last strategy I present in Pine Script (the language of TradingView). As much as I love charting on TV, I do not love their backtesting approach. It only tests one instrument at a time and needs a few features I would like my backtest software to have (such as knowing its own performance).

The ability to create your own indicators for charting is fantastic, despite the moderator nerds removing anything you publish that doesn’t fit their vague house rules. I’m not a fan of leaving things up to interpretation. As a general rule, humans suck, and when given just a little bit of power, it tends to corrupt. Leaving “rules” vague enough to be open to interpretation creates a power imbalance that is usually impossible to correct without a massive overhaul. Watch the news (any of it) if you want to see this play out in real time.

I’m done ranting… for now. ;)

Today, we have another simple strategy using, you guessed it, two of the three indicators we are studying. Before I get into the strategy criteria and the code, I will also talk (write) a bit about a platform I am currently playing with. If you have been following along, you know I don’t have any loyalty to a single platform. Nor have I been pleased with any of the ones I’ve used. I am well aware that the features and functions I am looking for in a backtesting platform may not exist, and I will likely have to write something myself, but that isn’t going to stop me from trialing some of them as I come across something interesting.

The piece of software I am currently playing with is RealTest. This wicked-cool piece of software is developed and maintained by Marsten Parker, an actual trader who uses the software he developed in his own research and trading. That alone is enough to catch my attention and get me interested enough to look at the software, and it should interest you too. No one likes an armchair quarterback. So far, I have had nothing but good experiences with my RealTest trial. The user forum is active, and Mr. Parker is very responsive to questions and ideas.

The software doesn’t work with intraday data, but that isn’t a big concern for me. The more I read and learn, the less I see intraday strategies being discussed. There could be multiple reasons for this, but I have to wonder if intraday strategies aren’t what quant’s typically look for. Or, I just haven’t looked hard enough. Either way, I’m excited to try this software out and see what happens.

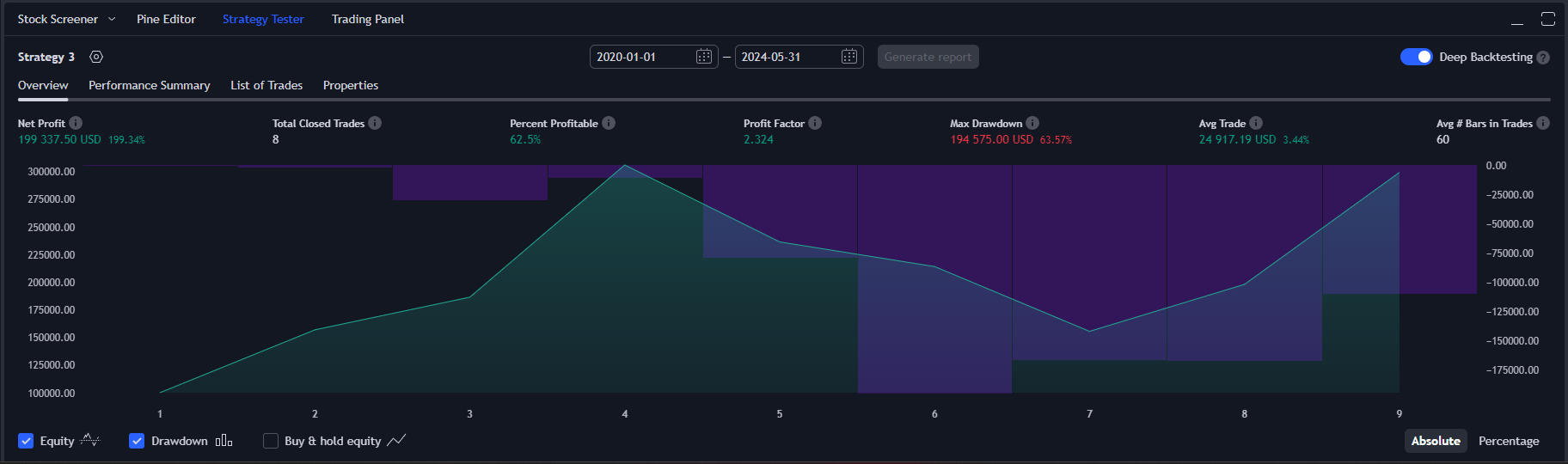

Backtest Results

This strategy is run on a daily chart. The following screenshots are results of the backtest on three different instruments: ES (S&P 500 futures contract), BTC/USDT (Bitcoin/USDTether), and SPY (S&P 500 ETF). The time period used for this test was 01/01/2020 to 05/31/2024.

ES (Daily, 01/01/2020 to 05/31/2024):

BTC/USDT (Daily, 01/01/2020 to 05/31/2024):

SPY (Daily, 01/01/2020 to 05/31/2024):

The strategy generates only a few trades and then holds them for a long period of time. It has two exit criteria, one of which is a type of trailing stop loss, and the other is an exit condition that utilizes one of the indicators. There is certainly room for improvement, but we can see that there is something here. With better exit criteria and trade management, this could be a decent, simple strategy to use in a trade system.

Simplicity

While we are on the subject of simplicity, I want to talk about another one of my core beliefs. I believe in keeping shit simple. When I first started working with ATS Research, one of the first things I brought up was a desire to tighten up each strategy (code it correctly) and then research the ones that perform well and see where they perform the best when they perform the best, and how to take advantage of that across a portfolio of strategies and instruments. I haven’t been with ATS Research for some time now, but I believe that is still the direction that Celan is taking the group. I always thought the “holy grail” was likely a strategy that used multiple strategies and chose which strategy was most appropriate for the moment.

This is (or appears to be) the same mentality that Marsten Parker (the guy who made RealTest) has. There is a quote from Parker in “Unknown Market Wizards” by Jack Schwager (did I mention that Parker was included in this book?):

It’s more effective to build a diverse collection of simple systems than to keep adding rules and re-optimizing a single system.

This quote is on the RealTest website’s landing page, and it aligns with my beliefs regarding simplicity. I do not believe this just because I am a trader; I have brought this concept into this field from my previous life as a paramedic and protective security specialist.

In my previous work, I met all sorts of cool people. Many of these “cool” people used to be Special Forces, Rangers, Navy Seals, or work for agencies that had groups with really cool names like “Ground Branch”. These guys were the subject matter experts. Certified bad asses. When you are around people with experience like that, you do everything you can to soak up the knowledge they have. I learned very quickly that there was only one secret, and once you embrace it, you can really improve your skills.

What is that secret?

Proficiency in the basics

Full stop.

I had to go through an “advanced pistol training” course once. This course was taught by an older SF gentleman. He started the class with a rant about how he hated naming any tactical course “advanced”. He told us the only thing that separated a high-functioning operator from a regular soldier/cop/enthusiast was practice. That’s it. The advanced pistol shooting course doesn’t teach you new pistol shooting skills; it just teaches you how to apply the same techniques in different scenarios, such as shooting from weird positions, around barriers/cover, or under stress.

This was nothing new for me. I have always embraced the Pareto Principle. As a paramedic, it is crucial to understand what will give you the most bang for your buck when treating a patient. Have a trauma patient? Stop the bleed and control the airway (in that order).

Bring it back to trading, Larry.

The point of all this is to say that I am going to continue to try to keep things simple. I don’t believe in overcomplicating things for no reason. Just like in tactical training, several basic skills can be applied together to make something appear more advanced than it really is. That is what I am going to work on building here: a library of diverse, simple strategies. This will lead to experimenting with multi-strategy systems and developing strategies that work across different asset types.

The rest of this post is for paid subscribers. Paid subscribers will have access to the private GitHub where all the Hunt Gather Trade code and strategies live. It is continuously being worked on and will expand as we explore the world of automated trade systems.