The Volatility Index -- Part 1

What is there to say? It's the VIX, broh. In three parts, and this is the first.

Disclaimer: the following post is an organized representation of my research and project notes. It doesn’t represent any type of advice, financial or otherwise. Its purpose is to be informative and educational. Backtest results are based on historical data, not real-time data. There is no guarantee that these hypothetical results will continue in the future. Day trading is extremely risky, and I do not suggest running any of these strategies live.

If you're reading this newsletter, you've likely heard about the VIX—often dubbed the market's "fear gauge." But what exactly is this index, and why do traders and economists keep such a close eye on it? As day traders, we are looking to answer two questions: can it be used to help our trade performance, or can its products be traded profitably?

In today's post, I plan on giving a explanation of what the VIX is, how traders use it, and what kinds of products can be used to trade the VIX itself. At the end, I propose some questions about the VIX that we will explore in the following posts. I am currently planning on a 3-part series, which will hopefully end with me being able to use the VIX or VIX products to design a simple trade strategy.

The CBOE Volatility Index

The VIX, or CBOE Volatility Index, is a real-time market index representing the market's expectations for volatility over the coming 30 days. In the words of the Chicago Board Options Exchange (CBOE):

"The VIX Index is a calculation designed to produce a measure of constant, 30-day expected volatility of the U.S. stock market, derived from real-time, mid-quote prices of S&P 500® Index (SPX℠) call and put options. On a global basis, it is one of the most recognized measures of volatility—widely reported by financial media and closely followed by a variety of market participants as a daily market indicator." 1

In simpler terms, the VIX gauges the level of fear or stress in the market. A high VIX value indicates that traders expect significant price swings (volatility) in the S&P 500 Index, while a low VIX suggests a calmer market environment.

How Is the VIX Calculated?

The broad strokes of calculating the VIX from the document involve the following key steps:

Selecting the Options: The VIX calculation uses near-term and next-term SPX and SPXW options. Specifically, AM-settled SPX options and PM-settled SPXW options are selected, excluding options expiring on the same day as AM-settled SPX contracts.

Calculating Interest Rates: The risk-free interest rates (R1 and R2) are calculated based on U.S. Treasury yields, interpolating to the relevant expiration dates.

Calculating Variances: For each selected option, the variance (σ²) is calculated using the midpoint of bid and ask prices, taking into account the time to expiration, the strike price, and the forward price (calculated based on call and put prices).

Final Calculation: The VIX index is computed by aggregating the contributions of each option. The final VIX value is derived by taking the square root of the 30-day weighted average of the near- and next-term variances, multiplied by 100.

This process results in a value representing the expected 30-day volatility of the S&P 500 Index. This information for this breakdown was pulled from the CBOE VIX White Paper.

How Do Traders Use It?

Traders and investors utilize the VIX in various strategic ways:

Risk Assessment: A rising VIX often signals increasing uncertainty or fear in the market. Traders might interpret a high VIX as a warning to exercise caution.

Hedging: Investors use VIX-related products to hedge against market downturns. Since the VIX typically moves inversely to the S&P 500, it can offset losses during market declines.

Speculation: Some traders engage in speculative activities by trading VIX futures and options, aiming to profit from volatility spikes.

Market Timing: By analyzing VIX trends, traders attempt to time their entry and exit points in the market.

How Is It Used on the Macroeconomic Scale?

On a broader scale, the VIX serves as a barometer for economic health:

Economic Indicators: Economists and policymakers monitor the VIX to gauge investor sentiment and potential economic turbulence.

Investment Decisions: Institutions may adjust their portfolios based on VIX levels to mitigate risk.

Policy Formulation: A consistently high VIX might influence central banks to implement measures to stabilize the economy.

How Do Traders Use It?

Traders and investors utilize the VIX in various strategic ways:

Risk Assessment: A rising VIX often signals increasing uncertainty or fear in the market. Traders interpret a high VIX as a warning to exercise caution, as it often correlates with market volatility or economic stress. According to Robert Whaley's analysis, the VIX is particularly effective in alerting investors to market shifts due to its sensitivity to implied volatility in SPX options.

Hedging: Investors use VIX-related products to hedge against market downturns. The VIX’s negative correlation with the S&P 500 makes it a suitable instrument for offsetting losses during periods of heightened market volatility. As documented in the CBOE methodology, VIX futures and options are designed to give traders direct exposure to volatility.

Speculation: Some traders engage in speculative activities by trading VIX futures and options, aiming to profit from volatility spikes. The ability to capitalize on sharp market movements, as highlighted by Whaley, makes the VIX a valuable tool for short-term traders.

Market Timing: By analyzing VIX trends, traders attempt to time their entry and exit points in the market. A high VIX is often interpreted as a sign of potential buying opportunities, while a low VIX might indicate a potential market peak.

How Is It Used on the Macroeconomic Scale?

On a broader scale, the VIX serves as a barometer for economic health:

Economic Indicators: Economists and policymakers monitor the VIX to gauge investor sentiment and potential economic turbulence. The CBOE Volatility Index often reflects global risk aversion, making it a key measure in economic forecasting. You will see market analysist such as mktcontext using the VIX alongside many other indicators and measures to help check the markets pulse.

Investment Decisions: Institutions may adjust their portfolios based on VIX levels to mitigate risk. As noted in Whaley’s research, the VIX’s ability to signal market stress allows institutional investors to reallocate assets more effectively during volatile periods. The VIX can be used to directly influence position sizing in trade systems that want to adjust for overall market volatility.

Policy Formulation: A consistently high VIX might influence central banks to implement measures to stabilize the economy, particularly during times of heightened financial uncertainty. Examples of this can be seen in the aftermath of Covid-19 and in early 2022 when the Federal Reserve began to tighten monetary policy in in response to rising inflation.

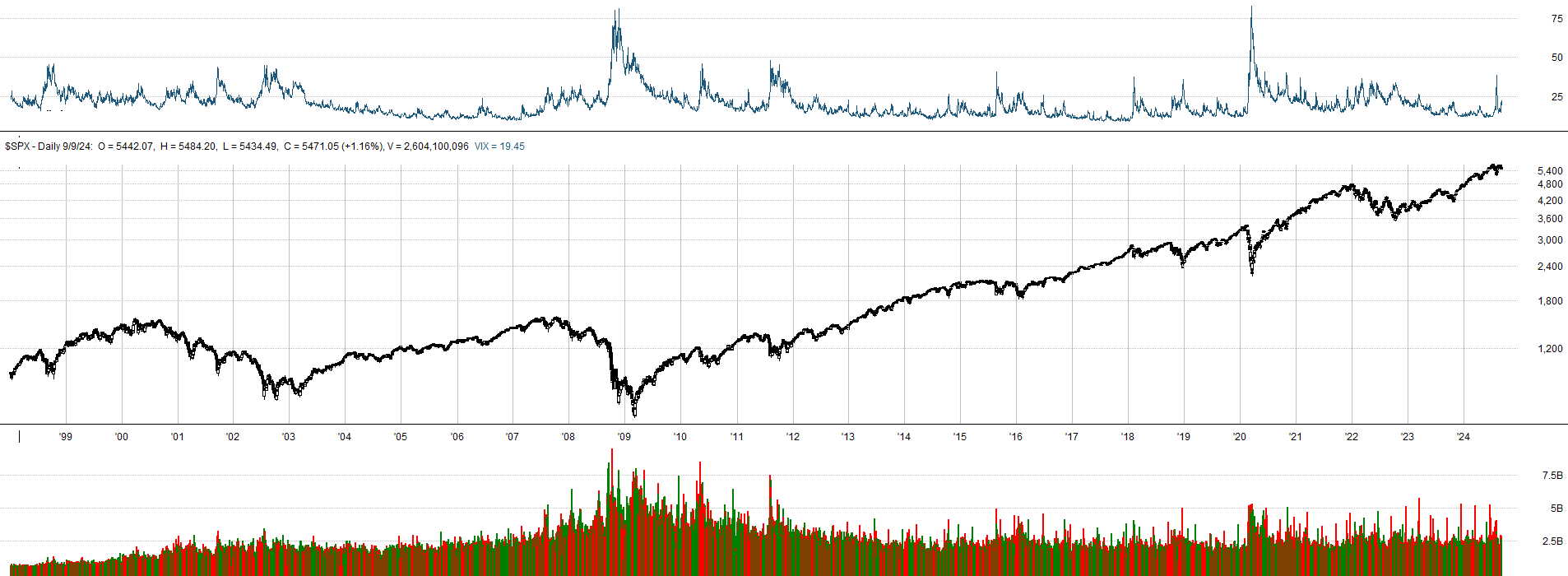

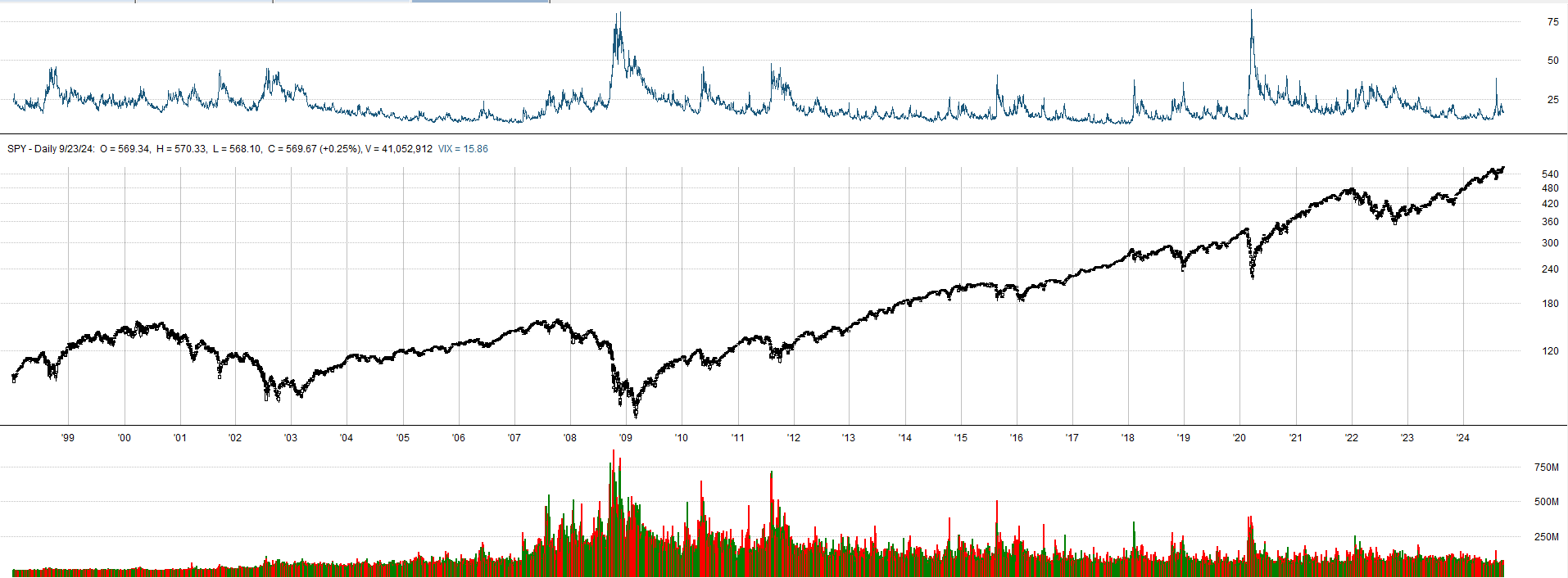

Example of VIX relationship to SPY/SPX

I threw this together into a RealTest scan just to see if I could eyeball the negative correlation. I would say that the relationship is pretty apparent. The relationship with volume is more pronounced on the SPY chart. The VIX charts are on top, the candlestick is SPX or SPY.

VIX/SPX:

VIX/SPY:

SPX/VIX Overlay:

The following correlation matrix/heatmap includes SH, TLT, and GLD to illustrate other examples of correlations with SPX and VIX. These assets represent an inverse equity ETF, long-term Treasury bonds, and gold, respectively, providing a broader perspective on how different asset classes interact with the stock market and volatility.

Gold has almost zero correlation with every asset included in this list, making it largely independent of the stock market and volatility index in this sample. Conversely, VIX and SH are highly positively correlated, meaning that both tend to increase when the stock market declines—VIX rises due to increased market volatility, and SH gains as an inverse ETF of the S&P 500. Of course, we see a strong negative correlation between SPX and VIX, indicating that as the S&P 500 index falls, market volatility typically rises.

Trading the VIX: Products and Instruments

VIX futures contracts (ticker symbol VX) are traded on the CBOE Futures Exchange and enable traders to speculate on the future value of the VIX. These contracts have expiration dates and can be used for hedging or speculative purposes. VIX options offer another avenue, allowing traders to buy or sell the right to trade VIX futures at a predetermined price before a specified date.

Exchange-Traded Products (ETPs) provide a more accessible way to trade volatility. Examples include:

iPath Series B S&P 500 VIX Short-Term Futures ETN (VXX**): An exchange-traded note that tracks the S&P 500 VIX Short-Term Futures Index Total Return.

ProShares VIX Short-Term Futures ETF (VIXY**): An ETF that seeks to provide exposure to short-term VIX futures, reflecting expectations of near-term volatility.

ProShares VIX Mid-Term Futures ETF (VIXM**): Focuses on mid-term VIX futures, offering exposure to volatility expectations over a longer horizon.

Considerations When Trading VIX-Related Products

Trading VIX-related instruments involves unique complexities. One key consideration is the concept of contango, where futures prices are higher than the spot price. This condition is common in VIX futures markets and can lead to a negative roll yield for ETPs that hold VIX futures. As these funds roll over expiring contracts into more expensive ones, their value can erode over time even if the VIX index remains stable.

Another factor is that VIX ETPs track VIX futures indexes, not the VIX index itself, which can result in performance differences due to the futures' term structure and pricing dynamics. Leveraged and inverse VIX products amplify exposure to volatility but come with increased risk, including the potential for significant losses if not managed carefully. These products are generally designed for short-term trading strategies rather than long-term investment.

Liquidity can also be a concern, as some VIX ETPs may have lower trading volumes, leading to wider bid-ask spreads and potential difficulties in executing large orders.

Exploring How the VIX Could Be Used in Trading Strategies

I’ve been considering different ways that the VIX could assist traders, particularly when it comes to managing risk and volatility in strategies involving S&P 500 constituents. While these are just some of the ideas I've been thinking about, I believe the VIX could offer valuable insights for filtering trades, adjusting position sizes, and even hedging portfolios. There may also be potential in using VIX products for pairs trading strategies. Below are a few of my thoughts on how the VIX could be applied within various trading approaches.

1. Volatility Filter for S&P 500 Strategies

The VIX might serve as a volatility filter to help traders decide whether to engage in a strategy based on overall market volatility. For example, elevated VIX levels could signal high market uncertainty, prompting a strategy to limit or avoid trades in S&P 500 stocks. On the flip side, a lower VIX might indicate more stable conditions, where trades could be executed with greater confidence.

2. Risk-Adjusted Position Sizing

Instead of relying on local volatility measures like a stock's ATR (Average True Range), traders could adjust position sizing based on broader market volatility reflected by the VIX. When the VIX is high, reducing position sizes can help manage risk across the board, while low VIX levels might justify taking larger positions in a less volatile market environment.

3. Using VIX to Hedge Market Exposure

VIX-related products could be used as hedging tools to protect against market downturns. In times of rising volatility, going long VIX futures, options, or ETFs like VXX could help offset losses in a broader portfolio, as the VIX typically spikes when the market declines. This way, traders could mitigate risk without needing to exit core positions.

4. Potential for Pairs Trading

There might also be opportunities to explore pairs trading using VIX-related products alongside other market indices or ETFs. For instance, a strategy could involve taking opposite positions in the VIX and SPY (or other S&P 500-linked instruments) to capitalize on the inverse relationship between volatility and market performance. This could allow traders to profit from market inefficiencies or changes in volatility expectations.

Conclusion

The next part of this series we are going to run the VIX and some of its different products through soundness testing. It isn't always necessary to test the instruments/markets that you intend to trade, but it isn't going to hurt either. It would be hard to trade a market that doesn't have stationary returns.

We will explore some of the relationships that we saw in our correlation matrix. As a side project, I am going to publish a video of using Python to get data from Norgate, shape it how we need it, and create a correlation matrix. I will go over the method used in this post, creating a heatmap image, and I will go over an unnecessary option for printing the correlation matrix to the terminal with color.

You read that right. It will look something like this:

Finally, I will also provide some methods for using the VIX as a trade filter and as a factor for risk-adjusted sizing.

Until next time.

Happy Hunting.

The code for strategies and the custom functions/framework I use for strategy development can be found at the Hunt Gather Trade GitHub. This code repository will house all code related to articles and strategy development. If there are any paid subscribers without access, please contact me via e-mail. I do my best to invite members quickly after they subscribe. That being said, please try and make sure the e-mail you use with Substack is the e-mail associated with GitHub. It is difficult to track members otherwise.

Feel free to comment below or e-mail me if you need help with anything, wish to criticize, or have thoughts on improvements. Paid subscribers can access this code and more at the private HGT GitHub repo. As always, this newsletter represents refined versions of my research notes. That means these notes are plastic. There could be mistakes or better ways to accomplish what I am trying to do. Nothing is perfect, and I always look for ways to improve my techniques.

References

Whaley, Robert E. "Understanding the VIX." Journal of Portfolio Management (2009): 98-105.