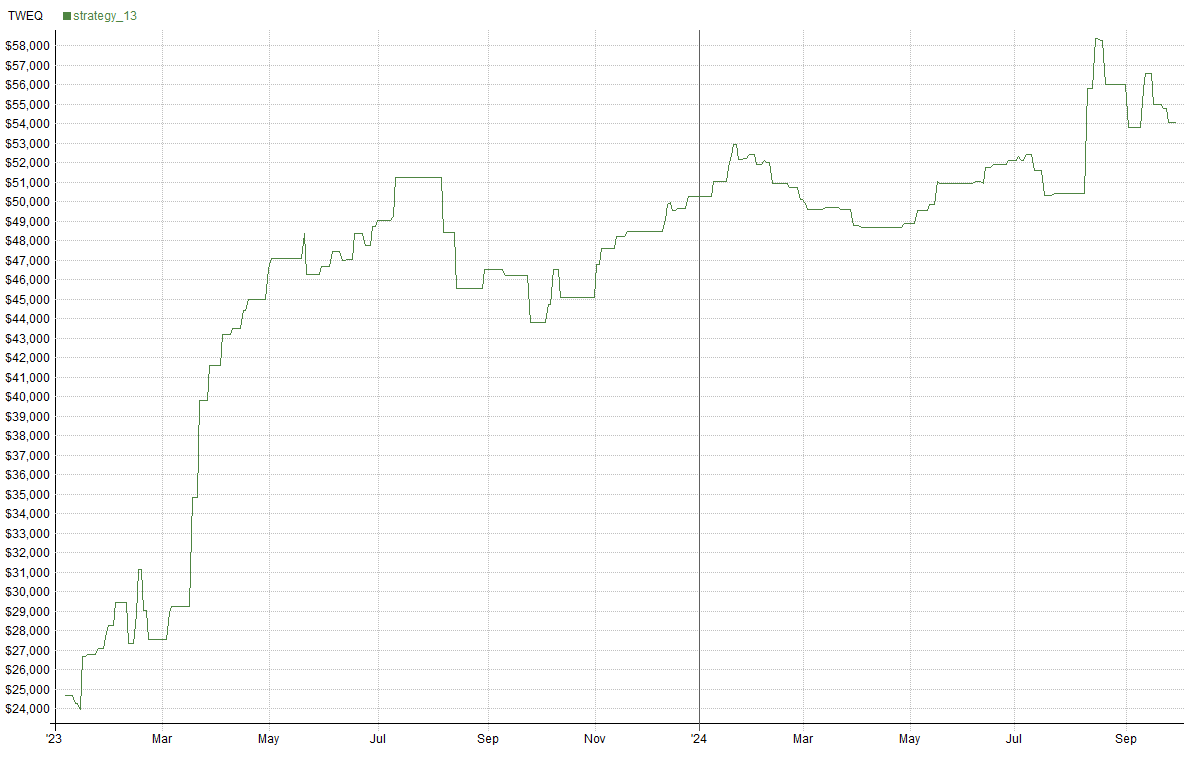

Strategy 13 -- A simple VIX futures trading strategy

A simple VX strategy with a PF of 1.8, Sharpe of 1.6, CAGR of 66%, and MaxDD -14%.

Disclaimer: the following post is an organized representation of my research and project notes. It doesn’t represent any type of advice, financial or otherwise. Its purpose is to be informative and educational. Backtest results are based on historical data, not real-time data. There is no guarantee that these hypothetical results will continue in the future. Day trading is extremely risky, and I do not suggest running any of these strategies live.

After the last strategy, I wanted to test the idea that you could use the activity of something like SPX (S&P 500 Index) and create a simple trading strategy to short VX (the VIX futures contract). This is what I came up with.

The Money Flow Indicator is used in this strategy. It is the only indicator used. This indicator is discussed in the post below:

Intraday Intensity and Chaikin's Money Flow

Disclaimer: the following post is an organized representation of my research and project notes. It doesn’t represent any type of advice, financial or otherwise. Its purpose is to be informative and educational. Backtest results are based on historical data, not real-time data. There is no guarantee that these hypothetical results will continue in the fu…

Summary Stats

Compound Annual Return: 66.67%

Max Historical Drawdown: -14.48%

Average Holding Period: 1 Day

Expectancy Per Trade: 0.59%

Win Rate: 66.77%

Profit Factor: 1.84

Sharpe Ratio: 1.67

MAR Ratio: 4.61